Revealed March 3, 2025

By Lindsay Fenlock, Senior Researcher on the Heart for Worldwide Environmental Regulation, and Charles Slidders, Senior Legal professional, Monetary Methods on the Heart for Worldwide Environmental Regulation, and Nikki Reisch, Director of the Local weather & Vitality Program on the Heart for Worldwide Environmental Regulation.

That is the fifth evaluation in a multi-part collection analyzing the intersection of the local weather emergency and the insurance coverage disaster.

The lethal fires that devastated Los Angeles and displaced a whole lot of 1000’s of individuals in January have been lastly contained, however they left one other kind of firestorm of their wake — one raging across the insurance coverage business and its shrinking protection of local weather dangers similar to excessive wildfires. Local weather change elevated the probability and severity of the fires — by far among the most damaging within the metropolis’s historical past. The blazes killed at least 28 individuals and destroyed some 16,000 constructions over almost 50,000 acres — an space bigger than the town limits of San Francisco. Insured property harm alone is anticipated to succeed in as a lot as $40 billion. The query of who pays looms massive.

For at the least fifty years, the insurance coverage sector has been conscious of the bodily dangers of local weather change and that greenhouse gasoline emissions, primarily from fossil fuels, are overwhelmingly answerable for rising temperatures. Regardless of this, US insurance coverage firms have investments of greater than $500 billion in fossil fuel-related belongings. The underwriting enterprise of main insurers stays closely centered on the fossil gas sector, with the highest US insurers of fossil gas companies incomes $5.2 billion from underwriting in 2023.

After many years of pocketing premiums from owners and investing vital parts of that cash within the fossil gas business that drives local weather change, personal insurers like State Farm and Berkshire Hathaway carved out hearth protection from their insurance policies or pulled out of the California market altogether.

The end result: The insurers that performed a task in facilitating the very local weather disasters now affecting their former clients have successfully lower and run, leaving the residents and the state holding the bag.

Non-public insurers will escape the complete invoice, largely as a result of they’ve shifted their publicity to probably the most excessive local weather dangers to California’s insurer of final resort — the FAIR Plan. In abandoning the California dwelling insurance coverage market, or in any other case excluding hearth protection from their insurance policies, personal insurance coverage firms successfully pushed the tasks of shouldering local weather threat again onto the general public and guarded their very own earnings. Regardless of their claims on the contrary, insurance coverage firms, as not too long ago as 2023, generated vital earnings on house owner insurance coverage insurance policies and are nonetheless raking in document earnings.

The FAIR Plan is now on the point of insolvency. To fund the shortfall, the California Insurance coverage Commissioner has levied an evaluation totaling $1 billion on personal insurance coverage firms. Nonetheless, personal insurance coverage firms will cross $500 million of the evaluation on to all of California’s insured owners.

This $500 million invoice is a direct consequence of local weather change and the profit-driven insurers who — after pocketing ever-increasing premiums and investing within the fossil gas sector — have shed insurance policies for properties most susceptible to local weather dangers. All of California’s dwelling insurance coverage policyholders are the victims of fossil-fueled local weather change.

Insurers Abandon Californians

The damaging pressure of the LA wildfires is a results of local weather change-induced drought, which led to the accumulation of dried-out vegetation and the right situations for excessive wildfires. Unusually sturdy wind gusts of greater than 100 miles per hour unfold the fires throughout LA, scattering flames all through lots of the metropolis’s communities. And it was not simply the fires inflicting harm — local weather change intensifies hearth smoke, filling the air with hazardous pollution that hurt well being.

In California, the frequency and severity of wildfires have elevated the price of disasters, prompting insurers to hike premiums or refuse to resume insurance policies. California’s dwelling insurance coverage charges jumped 48.4 p.c from 2019 to 2024. Twelve main insurers have additionally restricted owners insurance coverage even after being allowed huge charge hikes.

Insurers have justified abandoning California owners by citing rising local weather threat. But, insurance coverage firms are complicit in facilitating local weather change via their huge investments in fossil fuel-related belongings — together with coal, oil, and gasoline — the first sources of the greenhouse gases driving local weather change.

State Farm and the Hypocrisy of the Insurance coverage Sector

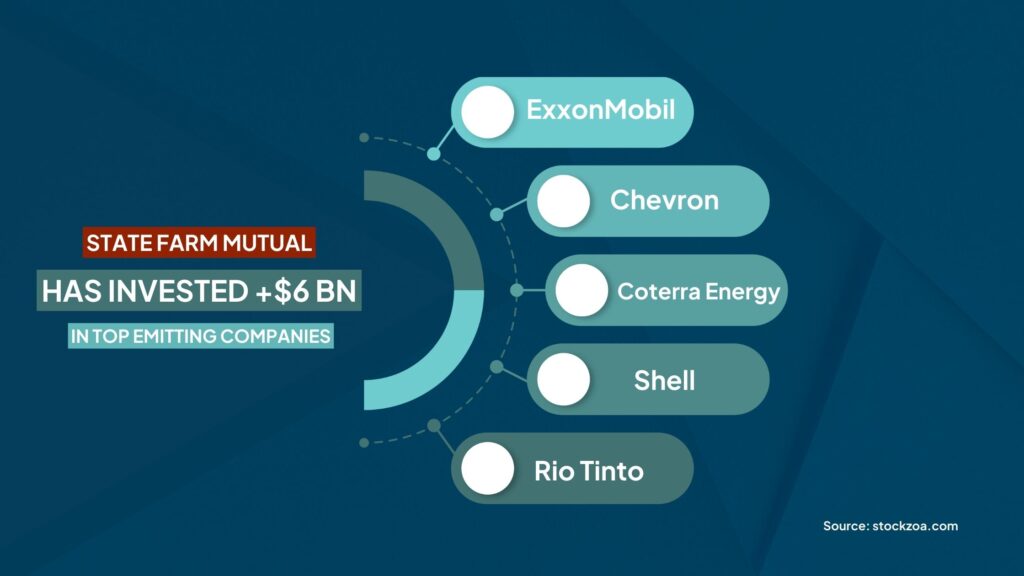

State Farm Common (State Farm) — via its mum or dad firm, State Farm Mutual — is a main investor in fossil fuels. The corporate’s investments embrace greater than $6 billion in upstream oil and gasoline producers ExxonMobil, Chevron, Coterra Vitality, and Shell and mining firm Rio Tinto. These 5 firms sit on the record of the highest investor-owned entities with the best historic carbon dioxide emissions. State Farm Mutual additionally has billions of {dollars} of investments in fossil-fuel-intensive or dependent industries similar to utilities, oil and gasoline companies, and pipeline firms, in addition to chemical, metal, and fertilizer producers.

Regardless of facilitating local weather change via its fossil gas investments, State Farm — the biggest property and casualty insurer in California — acknowledged in 2023 that it could not renew 30,000 dwelling insurance coverage insurance policies within the state. The choice was primarily because of the rising threat of wildfires in California. After an permitted charge enhance of 20 p.c in December 2023, amongst different concessions from the California Division of Insurance coverage, State Farm agreed to resume these 30,000 dwelling insurance coverage insurance policies, however solely on the situation that the renewed insurance policies exclude hearth protection. State Farm shoppers needed to particularly safe separate hearth protection from the FAIR Plan.

The Pacific Palisades, one of many neighborhoods devastated by the LA Fires, was one of many zip codes deserted by State Farm. In accordance with California Division of Insurance coverage spokesperson Michael Soller, State Farm dropped about 1,600 insurance policies in Pacific Palisades in July. State Farm additionally dropped greater than 2,000 insurance policies in two different LA zip codes, which embrace neighborhoods additionally broken by the wildfires, similar to Brentwood, Calabasas, Hidden Hills, and Monte Nido. The FAIR Plan is now the principal recourse for wildfire protection for former State Farm policyholders.

State Farm Calls for Fee Hike As an alternative of Utilizing Reinsurance Earnings

Most personal insurers need to their reinsurer to supply protection for his or her losses from the LA Fires. Reinsurance, principally insurance coverage for insurance coverage firms, is a typical a part of an insurer’s enterprise mannequin because it permits them to shift a few of their threat to guard themselves from probably the most catastrophic occasions. State Farm’s reinsurer is its mum or dad firm — State Farm Mutual. From 2014 to 2023, State Farm paid reinsurance premiums of almost $2.2 billion however was solely reimbursed $0.4 billion — lower than 20 p.c — suggesting that the corporate overpaid for reinsurance. These funds to its mum or dad firm, with little return, led to accusations that State Farm was artificially boosting its mum or dad firm’s earnings.

State Farm Mutual has over $130 billion in surplus out there to help its subsidiary. Regardless of the exorbitant earnings of its mum or dad firm and nicely earlier than the LA Fires, in June 2024, State Farm requested a 30 p.c enhance in its owners insurance coverage charges (on high of the 20 p.c enhance it was granted in March of the identical yr) purportedly to enhance its common monetary situation. Inside days of the LA fires being contained, State Farm once more requested its California policyholders to step in and keep the earnings of its mum or dad firm. State Farm requested an annual $740 million bailout within the type of an “pressing” 22 p.c enhance in State Farm’s dwelling insurance coverage charges, in addition to requesting charge hikes of 38 p.c for rental dwellings and 15 p.c for tenants.

Happily for California’s shoppers, Commissioner Ricardo Lara rejected State Farm’s requested charge enhance. And true to type, State Farm is now “contemplating its choices” as a result of the Commissioner’s determination “sends a robust message to State Farm Common concerning the help it is going to obtain to gather adequate premiums sooner or later” — a barely veiled menace to once more abandon California policyholders.

State Farm had already restricted its publicity to local weather change-induced wildfires after which sought to scale back it additional, asking policyholders to tackle much more of the remaining threat. All of the whereas, they proceed to facilitate local weather change and revenue from their fossil gas investments.

Local weather Change Pushes FAIR Plan to the Brink

As insurance coverage firms pull out of susceptible areas or increase premiums, many California owners are left with no selection however to depend on the FAIR Plan — the state-supported insurer of final resort. The FAIR Plan provides restricted protection at increased charges, making it pricey and an insufficient security web for owners deserted by personal insurance coverage firms.

The exit of insurers from the California residential property market has meant that the FAIR Plan’s publicity to wildfire threat has elevated exponentially. The FAIR Plan now holds 13,752 insurance policies with greater than $23 billion in legal responsibility throughout the residential and industrial sectors within the zip codes affected by the fires.

On February 11, 2025, Insurance coverage Commissioner Lara discovered “that the FAIR Plan is confronted with a considerable menace of insolvency on account of unprecedented losses” and permitted the FAIR Plan’s request to levy an evaluation totaling $1 billion on personal insurance coverage firms. Earlier than July 2024, insurers working in California would have been solely required to fund any deficit, paying a payment based mostly on their market share. However a July 2024 regulation permits insurers to shift 50 p.c of the evaluation onto the state’s current policyholders. Householders from throughout California are being requested to bail out the FAIR Plan, regardless of the danger profile of their dwelling and neighborhood and the local weather threat mitigation or adaptation they’ve undertaken.

This modification in regulation was a part of a collection of concessions Lara has given to the insurance coverage business lately, together with provisions that make it simpler for firms to increase premiums and a brand new rule that permits firms to make use of forward-looking disaster fashions when setting charges. These new rules have been geared toward convincing insurers to remain in California, however client advocates warn that they’ve the potential to additional exacerbate owners’ climate-related prices.

Making Insurers Tackle the Actual Perpetrator of Local weather Change

Insurance coverage firms facilitate local weather change by investing in fossil gas belongings and underwriting fossil gas tasks. Nonetheless, the first drivers of local weather change are fossil fuels themselves, and it’s the firms that produce and promote them which can be principally answerable for the local weather emergency. As an alternative of making an attempt to shift their publicity to California’s house owners, insurers ought to divest from fossil gas belongings and stop underwriting fossil gas tasks. Insurers ought to then search to recoup the prices of protecting the harm from local weather change-induced extreme climate occasions from fossil gas firms — not from the person policyholders or the general public at massive.

A brand new invoice, SB222, launched into the California legislature, would make it simpler to make sure that polluters pay for the climate-driven disasters befalling residents and upending the insurance coverage business. It particularly directs the FAIR Plan and incentivizes personal insurers to pursue the events answerable for local weather change-induced climate occasions by standing within the sneakers of policyholders to recoup the prices of losses, using their proper of subrogation. An insurer’s proper of subrogation is the suitable to attempt to get better the quantity of a declare or claims it paid out from one other occasion that precipitated the insured loss(es).

The draft laws directs the FAIR Plan to train its proper of subrogation in opposition to “a accountable occasion for a local weather catastrophe or excessive climate or different occasions attributable to local weather change” if the advantages of subrogation outweigh the prices (as decided by an impartial advisory physique). If the FAIR Plan’s funds are exhausted and personal insurance coverage firms are being assessed, as is the case now, the Invoice additionally offers incentives to insurers to train the suitable of subrogation in opposition to a “accountable occasion” for a local weather catastrophe. An insurer’s share of the evaluation will likely be lowered by 10 p.c if the insurer workout routines its proper of subrogation in opposition to a accountable occasion, but when it doesn’t train its proper of subrogation in opposition to a accountable occasion, it will likely be elevated by 10 p.c.

Lastly, along with its proper of subrogation, the Invoice offers that an insurer could search damages in opposition to a accountable occasion for a local weather catastrophe, excessive climate, or different occasions attributable to local weather change.

Make no mistake: the accountable events driving local weather change are fossil gas companies.

Insurers Should Cease Fanning the Flames of Local weather Threat

SB222 highlights that the actual offender of the local weather emergency is the fossil gas sector. However insurance coverage firms are removed from harmless bystanders. By supporting “enterprise as common” within the fossil gas sector, insurance coverage firms are facilitating the escalating local weather disaster, inflicting local weather change-induced occasions just like the LA fires. When coupled with their representations round defending policyholders from peril and their justifications for charge hikes and non-renewals, insurers’ conduct violates client safety legal guidelines and requirements.

Insurers should now not be permitted to take a position massive parts of premium revenue in fossil gas firms and underwrite new oil and gasoline tasks whereas charging some owners extra for elevated local weather threat and easily turning others away. Earlier than any additional handouts are given to the insurance coverage business or any extra concessions are made to protect a profit-driven insurance coverage mannequin that will merely be untenable within the age of local weather chaos, insurers should cease fanning the flames.